The Reserve Rule: How Much Cash to Hold Per Property (So You Don’t Go Broke)

Most real estate investors don’t fail because they bought the wrong property. The Reserve Rule: How Much Cash to Hold Per Property (So You Don’t Go Broke)

They fail because they ran out of cash at the wrong time.

The property didn’t kill them.

The market didn’t kill them.

The lack of reserves did.

If you want to stay in this game long enough to win, reserves are not optional. They are the difference between temporary pain and permanent exit.

This post gives you an evergreen rule. You can use it in any market, at any interest rate, with any strategy. This way, you won’t become another investor who “used to own rentals.”

Why Cash Reserves Matter More Than the Deal

Here’s the uncomfortable truth:

A great deal with weak reserves is a bad deal.

A mediocre deal with strong reserves can survive.

Real estate doesn’t break people all at once. It bleeds them slowly:

- Vacancy hits at the same time as a repair

- A tenant stops paying right after you replace the water heater

- Insurance goes up, taxes adjust, rent lags

- A roof waits patiently for your bank account to be empty

Cash reserves don’t increase returns.

They prevent forced decisions.

And forced decisions are where investors lose properties.

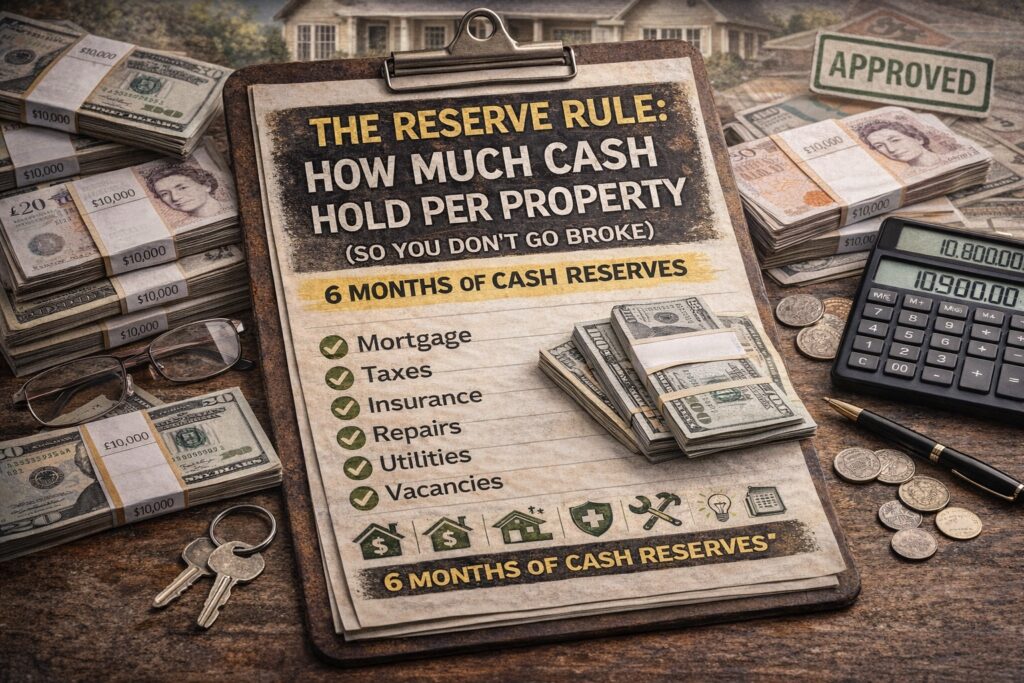

The Reserve Rule (Simple, Practical, Non-Negotiable)

Here’s the rule I use and recommend:

Per Property, Hold:

6 months of TOTAL operating expenses + debt service

Not just the mortgage.

Not just taxes and insurance.

Everything it costs to keep the property alive.

That includes:

- Principal & interest

- Taxes

- Insurance

- HOA (if applicable)

- Average maintenance

- Management (even if you self-manage)

This is your survival number.

If the property produces cashflow, great.

If it doesn’t—for six months—you’re still standing.

Why “3 Months” Is Usually a Lie

You’ll hear people say:

“Three months of reserves is fine.”

Three months assumes:

- no major repair

- no bad tenant

- no vacancy overlap

- no insurance or tax surprise

- no personal income disruption

That’s not conservative. That’s optimistic.

Real estate punishes optimism.

Six months gives you:

- time to re-tenant properly (not desperately)

- time to fix issues without panic

- time to ride out market noise

- time to keep your credit intact

The goal of reserves is not comfort.

It’s control.

The Real Reserve Buckets (This Is Where People Mess Up)

Smart investors separate reserves into buckets, even if it’s just mentally. The Reserve Rule: How Much Cash to Hold Per Property (So You Don’t Go Broke)

Bucket 1: Operating Reserves

This covers:

- mortgage

- taxes

- insurance

- HOA

- basic utilities (if owner-paid)

This is the “keep the lights on” money.

Bucket 2: Maintenance & CapEx

This is for:

- HVAC

- roof

- plumbing

- appliances

- electrical

- exterior work

If you don’t fund this monthly, you’re borrowing from your future self.

Bucket 3: Vacancy & Turnover

This covers:

- lost rent

- cleaning

- leasing fees

- minor rehab between tenants

Turnover is predictable over time. Treat it that way.

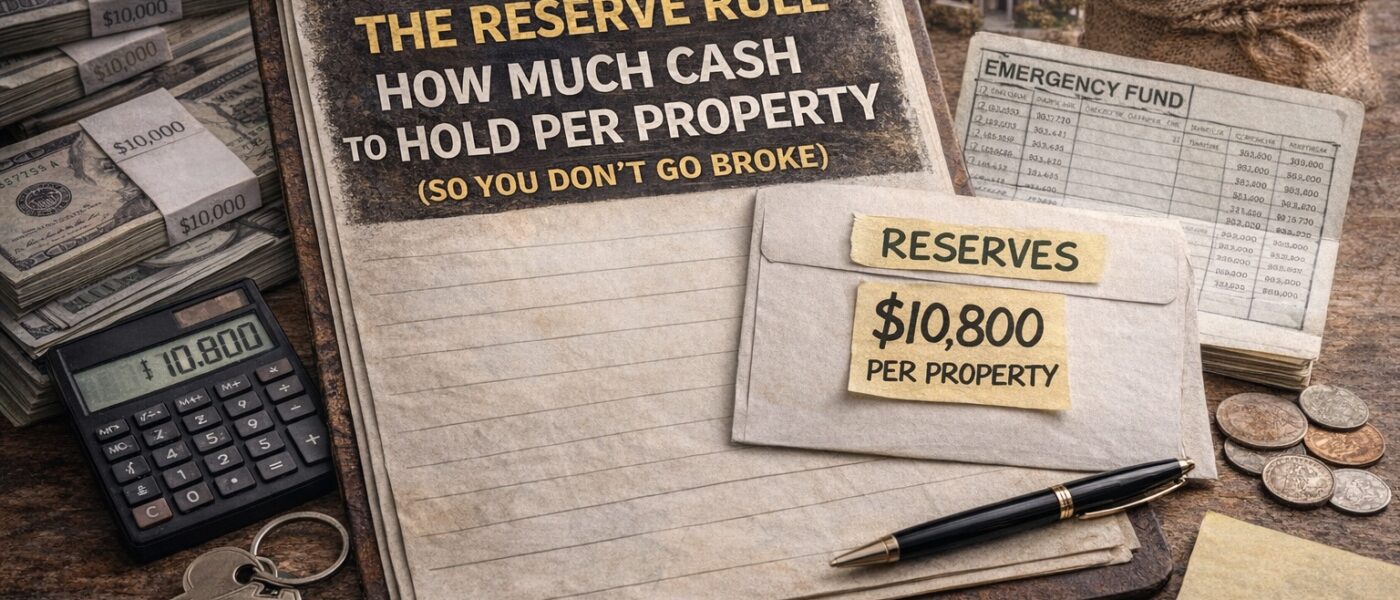

How Much Is Enough? (Real Numbers Example)

Let’s say a rental costs you $1,800/month all-in.

Your reserve target is:

- $1,800 × 6 = $10,800 per property

That number should exist before you buy the next deal.

Not after.

Not “I’ll build it up.”

Before.

This one rule alone prevents over-leveraging.

Where to Keep Reserves (Don’t Get Fancy)

Reserves are not for investing. They are for survival.

Keep them:

- liquid

- boring

- separate from personal spending

High-yield savings is fine.

Money market is fine.

Accessibility beats return every time.

If you have to think about how to access your reserves, they’re not reserves.

The Psychological Advantage Nobody Talks About

Strong reserves change how you operate:

- You negotiate better because you’re not desperate

- You can say no to bad tenants

- You can wait for the right contractor

- You sleep better

- You make long-term decisions

Cash doesn’t just protect your property.

It protects your judgment.

The Fastest Way Investors Blow Up

Here’s the pattern:

- Buy a property

- Use all cash for down payment + rehab

- “Rely on cashflow” to rebuild reserves

- Something breaks before reserves exist

- Credit cards fill the gap

- Stress rises

- Bad decisions follow

This is how “passive income” becomes a second job you hate.

The Hunter Rule (Write This Down)

Never buy your next property until your current property can survive six months without you.

That rule slows you down early.

But it keeps you in the game long enough to scale.

Final Truth

Cash reserves don’t make headlines.

They don’t look impressive on Instagram.

They don’t inflate returns on spreadsheets.

But they are the reason experienced investors are still standing when others disappear.

If you want real freedom from real estate, your first job is not to maximize cashflow.

Your first job is to make sure one bad season doesn’t take you out.

Support Hunter of Money — Build Freedom Tools for Everyday People