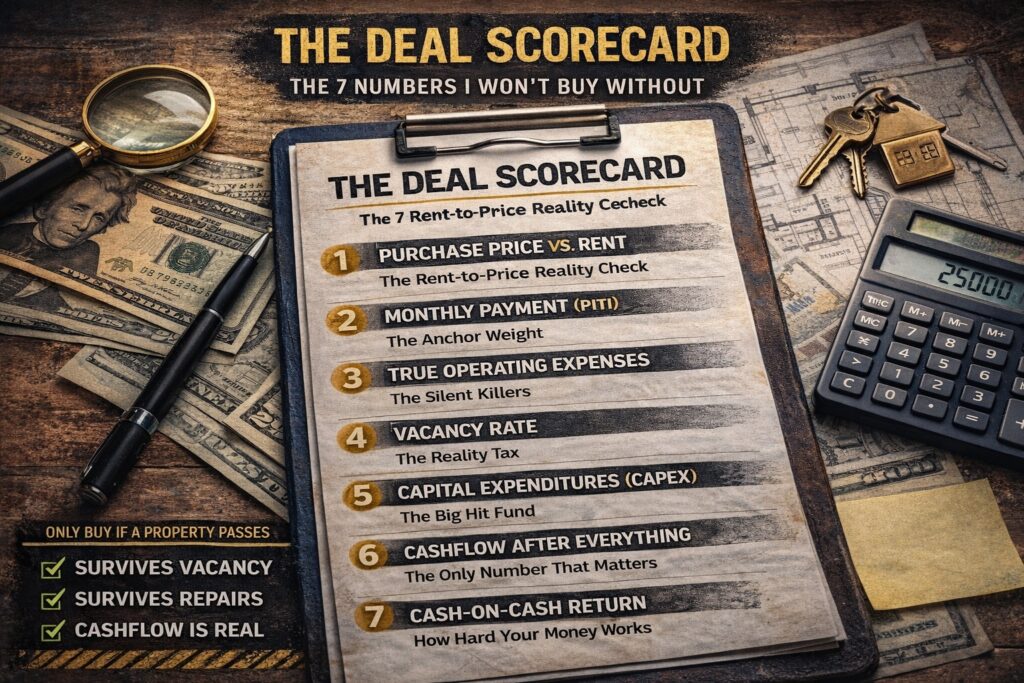

The Deal Scorecard: The 7 Numbers I Won’t Buy Without

Most people lose money in real estate for one reason: they buy a “house” instead of buying a deal. The Deal Scorecard: The 7 Numbers I Won’t Buy Without.

A house is emotional. A deal is math.

And I’m not saying the math has to be complicated. I’m saying it has to be honest—because real estate doesn’t punish you on day one. It punishes you on month six. The first repair hits. Then the first tenant goes quiet. The first vacancy shows up, and you realize your “cashflow” was fantasy.

This is the Deal Scorecard I use to protect myself from bad deals and to pinpoint good ones fast. Seven numbers. No fluff. No spreadsheets required (but you should use one).

The 7 Numbers

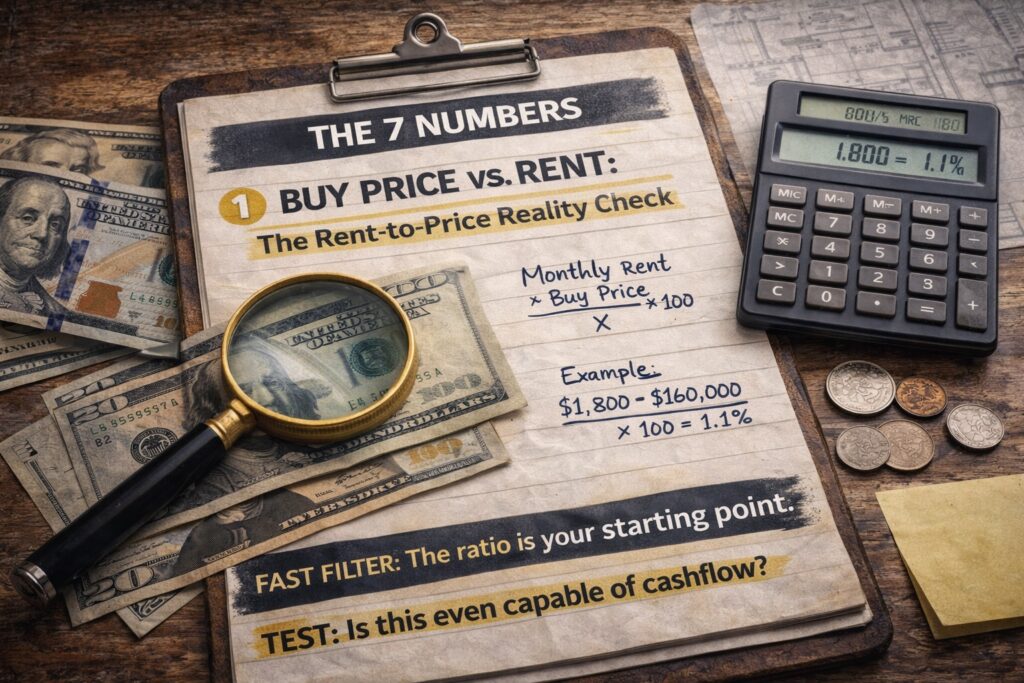

1) Buy Price vs. Rent: The Rent-to-Price Reality Check

Before anything else, I want to see if rent even has a chance to carry the deal.

Quick check:

- Monthly Rent ÷ Buy Price

- Multiply by 100 to get a rough percentage.

This isn’t “the rule.” It’s a smoke test.

If the rent-to-price ratio is too low, you’ll be fighting uphill. The debt payment and expenses won’t leave room for profit. In high-cost markets, this ratio is often low. So, cash flow investors either negotiate hard, add value, or choose a different market.

What it tells you:

Can this property become a cash flow asset? Or is it merely a “hope the price goes up” play?

2) Monthly Payment (PITI): The Anchor Weight

The mortgage doesn’t care about your optimism.

I calculate:

- Principal + Interest

- Taxes

- Insurance

That’s PITI.

This is the fixed weight you carry every month whether the property is rented or vacant.

Rule: If the payment is so high that one vacancy month would hurt you badly, the deal is fragile.

3) True Operating Expenses: The Silent Killers

This is where people lie to themselves.

Operating expenses aren’t just taxes and insurance. Real rentals bleed money quietly through:

- management (even if you self-manage, your time has value)

- maintenance

- utilities (sometimes)

- HOA

- lawn care

- pest control

- admin costs

- leasing fees

A practical approach is to estimate operating expenses as a percentage of rent, then refine with real quotes.

What it tells you:

Whether cashflow is real or imaginary.

4) Vacancy Rate: The Reality Tax

Vacancy is not “if.” It’s “when.”

Even the best market has vacancies:

- tenant turnover

- repairs between tenants

- seasonal slowdowns

- problem tenants that need removal

You have to assign vacancy a number.

Simple rule:

Assume at least 5% vacancy as a baseline. More if the area is unstable or the tenant base is high turnover.

What it tells you:

If the deal survives real life, not perfect life.

5) Capital Expenditures (CapEx): The Big Hit Fund

CapEx are the big-ticket items that don’t happen every month but will happen eventually:

- roof

- HVAC

- water heater

- plumbing

- electrical

- exterior paint

- driveway

- major appliances

If you don’t fund CapEx monthly, you will pay for it later… in pain.

Rule: Put aside a CapEx amount per month—based on property age and condition.

What it tells you:

Whether you’re building a durable asset or a ticking time bomb.

6) Cashflow After Everything: The Only Number That Matters

Now we bring it together.

Cashflow = Rent – (PITI + Operating Expenses + Vacancy + CapEx + Management)

Not rent minus mortgage. The Deal Scorecard: The 7 Numbers I Won’t Buy Without.

If cashflow is weak, the deal is weak. Period.

My mindset:

If cashflow can’t survive conservative assumptions, I don’t buy it.

Because I’m not buying to “break even.” I’m buying to build freedom.

7) Cash-on-Cash Return: How Hard Your Money Works

Cashflow is monthly. Cash-on-cash is the annual performance of the cash you invested.

Cash-on-Cash = Annual Cashflow ÷ Total Cash Invested

Total cash invested includes:

- down payment

- closing costs

- repairs/rehab

- initial reserves (if you’re disciplined)

What it tells you:

Whether this deal beats other options—like index investing, dividends, or just waiting for a better opportunity.

The Deal Scorecard (simple pass/fail)

Here’s the brutal truth: you don’t need perfect numbers. You need a deal that passes minimum survival thresholds.

A deal must pass:

- Cashflow stays positive even with conservative expense/vacancy assumptions

- Reserves are realistic (you can survive repairs + vacancy)

- Cash-on-cash return makes sense vs alternatives

- Exit options exist (sell, refinance, rent different strategy)

If it fails, you walk. Walking is a skill.

Common Ways People Trick Themselves (and go broke)

1) “I’ll self-manage so management is zero.”

No. If you self-manage, either:

- you pay yourself in time, or

- you eventually pay someone in money.

Put a number in.

2) “Vacancy won’t happen.”

Vacancy is guaranteed over time. The question is whether you planned for it.

3) “CapEx won’t hit for a while.”

That’s what everybody says right before the HVAC quits.

4) “It’ll appreciate.”

Maybe. But appreciation won’t pay your mortgage next month.

How This Connects to Your Wealth Plan

If you’re building wealth the Hunter way, this scorecard becomes your filter.

- Index ETFs build steady wealth in the background

- Dividends build cashflow and patience

- Real estate is the accelerator when the deal is real

But you don’t accelerate into a wall.

You buy deals that survive reality.

Your Next Step: Use This Scorecard on a Real Property Today

Pick any listing in your market and run it through the 7 numbers.

If you want, paste these into a message:

- purchase price

- expected rent

- taxes + insurance estimate

- HOA (if any)

- property condition (roof/HVAC age if known)

And I’ll score it with you.

Support Hunter of Money — Build Freedom Tools for Everyday People